DeFi Grew Up. It Just Doesn't Have Its Name on the Door.

By Harry Alford Guest Author Updated June 11, 2026

Summary

- DeFi infra companies are quietly becoming the backend layer helping neobanks offer crypto-powered savings and earn products

- Most users do not care about the crypto rails underneath they just want higher yields and a seamless savings experience

- As neobanks and RWAs grow into trillion-dollar markets, infra providers could become the most important layer in onchain finance

The following is a guest article by Harry Alford, ecosystem contributor and DeFi commentator closely associated with the Monad Foundation, where he regularly writes about the future of onchain finance, consumer crypto applications and DeFi infrastructure.

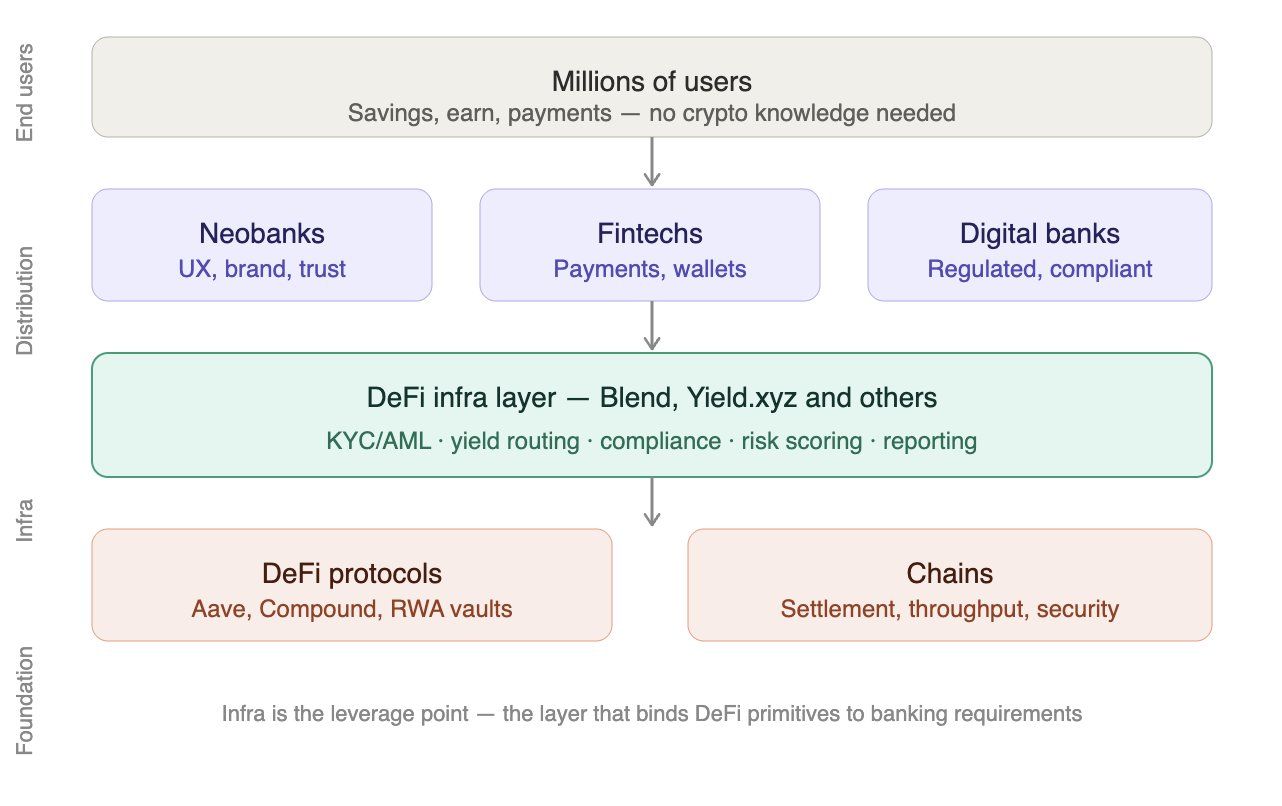

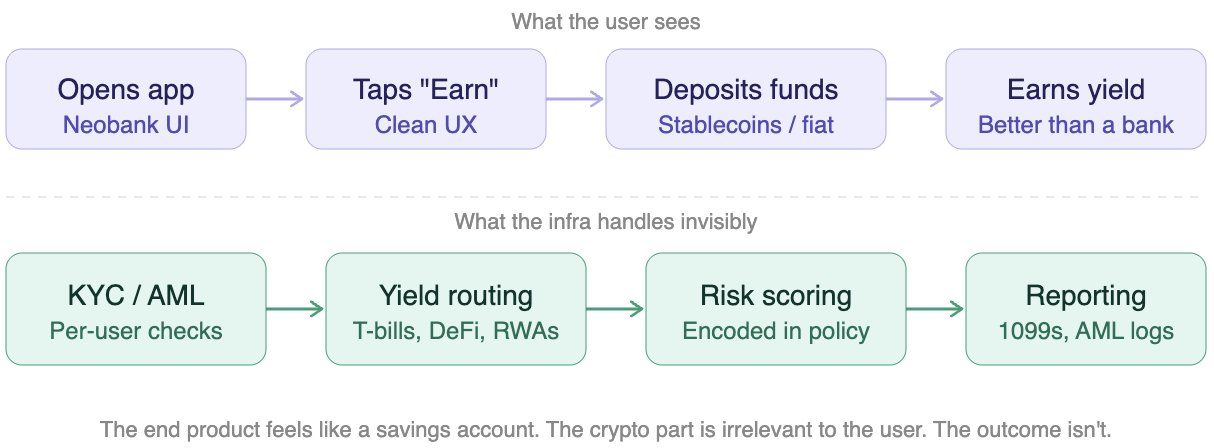

The Hidden Layer Helping Neobanks Go DeFi

When people say "DeFi meets TradFi," they picture JP Morgan on a blockchain. The real story is less glamorous and more important.

A new layer of DeFi infra companies is quietly powering neobanks from behind the scenes. They're not trying to be consumer brands. They're building the pipes, compliance rails, and risk frameworks that let other products ship "earn" and "savings" features that look like traditional banking but are backed by DeFi and RWAs.

From Protocol To Plumbing

Early DeFi was monolithic: Aave, Compound, Maker. Each with its own UI, users, and liquidity campaigns. Now the shift is toward infra-focused players whose entire job is to enable other businesses. They abstract away chain routing and bridging, normalize access to onchain liquidity and tokenized funds, handle KYC and AML at scale, and provide the SLAs that real businesses can actually rely on.

DeFi TVL hit $237B in 2025 and the RWA market grew 380% in three years. That layer didn't exist in DeFi 1.0. Now it does.

Who's Doing It

There are a few players doing this with @blend_money being one of them. Blend is a white-label earn infrastructure built for neobanks. Each end user gets their own self-custodial smart contract account. Funds aren't co-mingled, and they remain accessible onchain even if the platform disappears.

Blend has purpose-built earn pages with T-bill yields and DeFi lending, risk ratings translated into language compliance officers actually understand, and KYC, AML, and 1099s all handled out of the box. It's productizing the messy middle between DeFi protocols and the neobanks that want to use them.

Why Neobanks Want This

Neobank founders across geographies and audiences keep running into the same wall: they can't be DeFi engineers and a regulated bank at the same time. Compliance is non-negotiable. Integration costs kill experimentation. Mistakes around smart contracts or risk selection are existential.

So infra players step in:

"We'll handle the chains, protocols, bridges, KYC vendors, and reporting. You focus on customers."

That's the unlock.

What Users Actually Want

For all the complexity underneath, what end users want is straightforward. Stable returns and a seamless experience. They want something that looks and feels like a savings account but pays a better yield than their bank. The "crypto" part is irrelevant to them. The outcome isn't.

That gap between what users want and what raw DeFi actually delivers is exactly where infra companies live. They absorb the complexity so the end product feels boring in the best possible way.

The Thesis

Protocols are essential but increasingly interchangeable. Chains provide performance but need usage. Neobanks own UX, brand, and customer trust. DeFi infra is the leverage point that binds it all together, translating between DeFi primitives and banking requirements, encoding compliance into reusable services, and turning onchain finance into something that can clear a risk committee, not just attract degen capital.

Over 400M people worldwide now use neobanks, with the sector projected to surpass $6.5T in deposits by 2030. Standard Chartered projects the RWA market could reach $30 trillion by 2034. The question is no longer whether this is real; it's who's building the pipes.

If the next phase of this industry is millions of people holding digital asset savings and moving value on stablecoin rails without knowing or caring it's crypto, the infra companies will be the ones that made it possible. Perfectly happy to let someone else put their logo on the home screen.

This article was originally published on X by @HarryAlford3.

Join the Beluga Brief

Dive deep into weekly insights, analysis, and strategies tailored to you, empowering you to navigate the volatile crypto markets with confidence.

Never be the last to know

and follow us on X