AI Agents Can Now Pay. But Can We Trust Them?

By Pratik Bhuyan Updated June 1, 2026

Summary

- Agentic finance is becoming less about moving money and more about establishing trust, accountability, and control over autonomous systems.

- x402 is quickly emerging as a common payment rail, turning agent payments into shared infrastructure rather than a competitive edge.

- As payment rails mature, the focus is shifting toward wallets, governance frameworks, and safeguards for AI-controlled funds.

Introduction

If you spend enough time around crypto and AI, you'll hear a familiar prediction: AI agents are about to become economic actors.

They'll book flights, buy data, hire freelancers, subscribe to services, trade assets, and pay other agents without a human approving every step.

That raises an obvious question: how do they pay?

For the last year, most of the attention in agentic finance has focused on that problem. Startups rushed to build payment rails. Stablecoin companies launched agent products. Investors poured billions into infrastructure designed for machine-to-machine commerce.

The payment problem is starting to look solved. But something interesting happened along the way. The harder challenge is figuring out who is responsible when an AI agent starts moving money on behalf of a person or business.

And that is where the real battle is beginning.

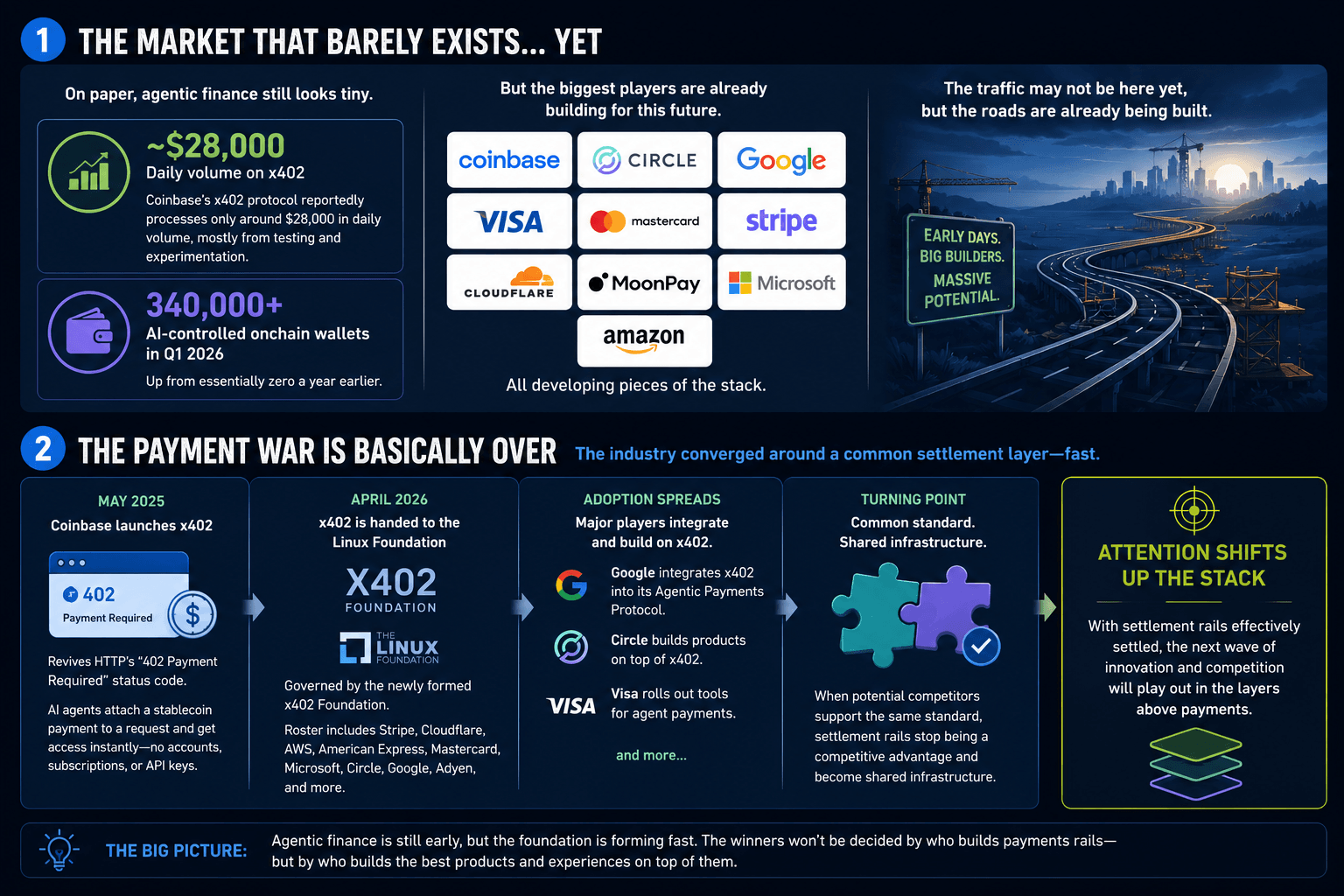

The market that barely exists... yet

On paper, agentic finance still looks tiny. Coinbase's x402 protocol, one of the most widely discussed payment standards for AI agents, reportedly processes only around $28,000 in daily volume. Much of that comes from testing and experimentation rather than real commerce.

Yet some of the world's biggest companies are already building for this future. Coinbase, Circle, Google, Visa, Mastercard, Stripe, Cloudflare, MoonPay, Microsoft, and Amazon are all developing pieces of the stack.

The reason becomes clearer when you look at another number. More than 340,000 onchain wallets were reportedly controlled by AI agents during the first quarter of 2026. Just a year earlier, that number was essentially zero.

The traffic may not be here yet, but the roads are already being built.

The payment war is basically over

The biggest surprise in this sector is how quickly the industry converged around a common settlement layer.

In May 2025, Coinbase launched x402, a protocol that revives HTTP's old "402 Payment Required" status code. Instead of creating accounts, managing subscriptions, and generating API keys, an AI agent can simply attach a stablecoin payment directly to a request and receive access instantly.

By April 2026, Coinbase handed x402 to the Linux Foundation, where it became governed by the newly formed x402 Foundation. The roster includes Stripe, Cloudflare, AWS, American Express, Mastercard, Microsoft, Circle, Google, Adyen, and several other major players.

Adoption spread surprisingly quickly. Google integrated x402 into its Agentic Payments Protocol, Circle began building products on top of it, and Visa rolled out its own tools for agent payments.

That's usually the point where a technology stops being a competitive advantage and starts becoming shared infrastructure. When companies that could be building rival systems instead choose to support the same standard, the battle over settlement rails is effectively settled.

As a result, the industry's attention is already shifting to the layers above payments, where the next wave of competition is likely to emerge.

The stack for machine commerce is already forming

Once payment rails become standardized, value shifts to the layers built on top of them.

The first layer is custody. AI agents need somewhere to hold assets and sign transactions securely. Businesses are understandably reluctant to hand unrestricted private keys to autonomous software.

- MoonPay's answer is the Open Wallet Standard, launched in March 2026 with backing from PayPal, Circle, Ripple, OKX, the Ethereum Foundation, and the Solana Foundation. The goal is simple: give agents a common wallet framework that works across multiple blockchain ecosystems without exposing private keys.

- Circle's Agent Stack bundles agent wallets, a marketplace for discovering services, developer tools, and Nanopayments, a system that enables transfers as small as one-millionth of a dollar using USDC. That may sound excessive until you consider how machines transact.

Humans might make a few purchases a day. AI agents could make thousands. A research agent might buy tiny pieces of data from dozens of providers. An automated trading system could continuously pay for analytics, models, and information feeds.

Traditional payment networks were never designed for millions of sub-cent transactions. MoonPay is tackling the spending side of the equation. Its MoonAgents Card allows AI agents to use stablecoins at any merchant that accepts Mastercard, connecting machine-controlled wallets to the existing payments ecosystem.

When you zoom out, what's striking is how many of the core building blocks are already in place. Agents can securely hold assets, discover and pay for services, handle tiny transactions at scale, and even spend money in the real world.

The vision of machine-to-machine commerce may still be in its early stages, but from a technical standpoint, much of the infrastructure needed to support it is already being built.

The real problem: who's responsible?

This is where things get complicated. Imagine an AI agent managing part of a company's treasury that accidentally sends $100,000 to the wrong vendor, pays a fraudulent counterparty, or violates internal compliance policies. Who is responsible when that happens? Is it the company that deployed the agent, the developer who built it, the wallet provider that enabled the transaction, or the AI model itself? The answer remains unclear, and that uncertainty may be the biggest obstacle facing agentic finance today.

This is exactly the problem Catena Labs is trying to solve. Founded by Circle co-founder Sean Neville, Catena raised $30 million in May 2026 and applied for a national trust bank charter with the U.S. Office of the Comptroller of the Currency (OCC). Unlike most companies in the sector, Catena is not focused on helping agents move money faster.

Instead, it is focused on helping businesses trust agents with money in the first place. Its platform allows organizations to establish spending limits, approved counterparties, balance restrictions, and oversight mechanisms before agents gain access to funds. In other words, Catena is building governance rather than payments - and that distinction could prove far more important.

Why the OCC matters more than another protocol launch

For most of crypto's history, regulation has been seen as a constraint on innovation. In the case of agentic finance, however, it may end up being an enabler.

The GENIUS Act, signed into law in 2025, established the first federal framework for payment stablecoins in the United States. Attention is now turning to July 18, 2026, when the OCC is expected to finalize a new set of stablecoin rules that could have important implications for AI-driven financial systems.

One proposal would allow permitted stablecoin issuers to transact either as principals or on behalf of others. While that may sound like a technical legal distinction, it touches on one of the core questions behind agentic finance: how should the law treat systems that are designed to move money on someone else's behalf?

What actually matters from here

Agentic finance has largely been framed as a payments story. That made sense when the industry was still figuring out how autonomous systems could hold assets, send transactions, and pay for services without human intervention.

But payments are increasingly becoming infrastructure rather than a point of differentiation. x402 is emerging as a common settlement rail, wallet standards are taking shape, micropayment systems are live, and card networks already provide a bridge into the traditional economy.

As those pieces fall into place, the harder questions move higher up the stack:

- Who controls an agent?

- Who is accountable when it makes a mistake?

- What guardrails govern its behavior?

- And who can regulators ultimately hold responsible?

Those questions are less exciting than instant payments and autonomous commerce, but they're also where much of the long-term value is likely to be created.

Our key takeaway is that the winners in agentic finance probably won't be the companies building better payment rails. They'll be the companies that answer a much harder question: How do you trust an AI agent with real money?

That's why one of the most important developments in agentic finance right now isn't another protocol launch. It's the OCC's eventual decision on Catena's bank charter.

If you liked this article, it’s time to level up. Get the Best Free Crypto Newsletter now! Insightful. Curated. Essential ~ The Beluga Brief.

Join the Beluga Brief

Dive deep into weekly insights, analysis, and strategies tailored to you, empowering you to navigate the volatile crypto markets with confidence.

Never be the last to know

and follow us on X